Besplatna dostava putem Box Now paketomata i Overseas kurirske službe iznad 59,99 €!

Besplatna dostava Overseas kurirskom službom iznad 59.99 €

Overseas 4.99 €

Pošta 4.99 €

DPD 5.99 €

GLS 3.99 €

GLS paketomat 3.49 €

Box Now 4.49 €

Kako kupovati

Kako kupovati

Pomoć

Dostava

Overseas 4.99 €

Pošta 4.99 €

DPD 5.99 €

GLS 3.99 €

GLS paketomat 3.49 €

Box Now 4.49 €

Besplatna dostava Overseas kurirskom službom iznad 59.99 €

Savjetnik za kupnju

Ovdje smo zbog vas!

+385 21 784 0072

Moj račun

Pridružite se zajednici ljubitelja knjige iz cijelog svijeta i ostvarite mnoštvo pogodnosti.

Izradite besplatni račun

▸

Prazno :-(

0

Besplatna dostava putem Box Now paketomata i Overseas kurirske službe iznad 59,99 €!

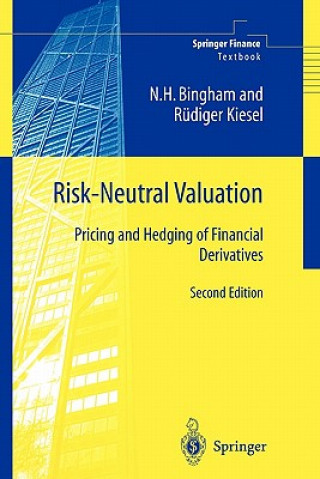

Risk-Neutral Valuation

Jezik

Engleski

Engleski

Engleski

Knjiga

Meki uvez

This second edition - completely up to date with new exercises - provides a comprehensive and self-c...

Cijeli opis

Libristo kod: 01434764

?

195 b

195 b

195 b

77.48

€

Vanjske zalihe u manjem broju

Šaljemo za 13-16 dana

30 dana za povrat kupljenih proizvoda

Moglo bi vas zanimati i

/

List

/

List

11.76

€

11.76

€

This second edition - completely up to date with new exercises - provides a comprehensive and self-contained treatment of the probabilistic theory behind the risk-neutral valuation principle and its application to the pricing and hedging of financial derivatives. On the probabilistic side, both discrete- and continuous-time stochastic processes are treated, with special emphasis on martingale theory, stochastic integration and change-of-measure techniques. Based on firm probabilistic foundations, general properties of discrete- and continuous-time financial market models are discussed.

Informacije o knjizi

Puni naziv

Risk-Neutral Valuation

Jezik

Engleski

Engleski

Uvez

Knjiga - Meki uvez

Datum izdanja

2010

Broj stranica

438

EAN

9781849968737

ISBN

184996873X

Libristo kod

01434764

Nakladnici

Springer London Ltd

Težina

682

Dimenzije

158 x 233 x 24