Besplatna dostava putem Box Now paketomata i Overseas kurirske službe iznad 59,99 €!

Besplatna dostava Overseas kurirskom službom iznad 59.99 €

Overseas 4.99 €

Pošta 4.99 €

DPD 5.99 €

GLS 3.99 €

GLS paketomat 3.49 €

Box Now 4.49 €

Kako kupovati

Kako kupovati

Pomoć

Dostava

Overseas 4.99 €

Pošta 4.99 €

DPD 5.99 €

GLS 3.99 €

GLS paketomat 3.49 €

Box Now 4.49 €

Besplatna dostava Overseas kurirskom službom iznad 59.99 €

Savjetnik za kupnju

Ovdje smo zbog vas!

+385 21 784 0072

Moj račun

Pridružite se zajednici ljubitelja knjige iz cijelog svijeta i ostvarite mnoštvo pogodnosti.

Izradite besplatni račun

▸

Prazno :-(

0

Besplatna dostava putem Box Now paketomata i Overseas kurirske službe iznad 59,99 €!

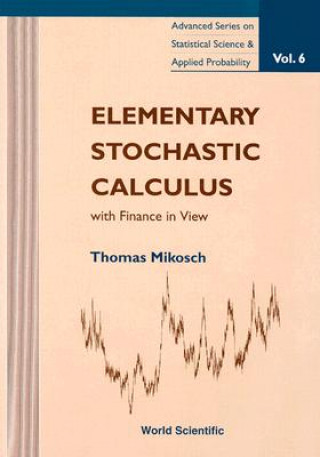

Elementary Stochastic Calculus, With Finance In View

Jezik

Engleski

Engleski

Engleski

Knjiga

Tvrdi uvez

Modelling with the Ito integral or stochastic differential equations has become increasingly importa...

Cijeli opis

Libristo kod: 04342370

?

168 b

168 b

168 b

67.22

€

Vanjske zalihe

Šaljemo za 3-5 dana

30 dana za povrat kupljenih proizvoda

Moglo bi vas zanimati i

/

Meki uvez

/

Meki uvez

16.97

€

16.97

€

/

Meki uvez

42.86

€

/

Meki uvez

42.86

€

Modelling with the Ito integral or stochastic differential equations has become increasingly important in various applied fields, including physics, biology, chemistry and finance. However, stochastic calculus is based on a deep mathematical theory. This text should be suitable for the reader without a deep mathematical background. It seeks to provide an elementary introduction to that area of probability theory, without burdening the reader with a great deal of measure theory. Applications are taken from stochastic finance. In particular, the Black-Scholes option pricing formula is derived.

Informacije o knjizi

Puni naziv

Elementary Stochastic Calculus, With Finance In View

Jezik

Engleski

Engleski

Uvez

Knjiga - Tvrdi uvez

Datum izdanja

1998

Broj stranica

224

EAN

9789810235437

ISBN

9810235437

Libristo kod

04342370

Nakladnici

World Scientific Publishing Co Pte Ltd

Težina

474

Dimenzije

163 x 224 x 20